Once Canadian investors reach their mid-50s there are big gaps in how much money the average Canadian has in their Tax-Free Savings Account (TFSA). The TFSA only began in 2009, for one thing. In comparison to other retirement accounts that usually take decades to grow, this one is still pretty new.

This not only gave investors in their mid-50s less room to contribute over their lifetimes than younger generations, but it also meant that they suddenly had to deal with a lot of big expenses like mortgages and childcare costs.

Things that affect contributions

There are two main things to think about: how Canadians use the TFSA and how much they can put in. To see long-term growth in your TFSA, you need to make regular contributions and choose investments that can grow over time.

That’s a big difference when it comes to income levels. People with higher incomes can give more and, as a result, invest more aggressively.

In contrast lower-income families use the TFSA as a short-term savings buffer. This makes it easy to tell the difference between TFSAs that keep growing and those whose balances are often taken. Unused TFSA contribution room is still one of the main reasons why there is such a big difference between the average and potential account sizes.

This brings us to the next point: how do most Canadians use their TFSA? For a lot of people, the account is like a savings account where they keep cash or put it into a GIC. This can make long-term growth harder, especially when interest rates are low.

How your choices about investing affect long-term growth

TFSAs with a lot of cash grow slowly. Even when interest rates go up, like they have in the past few years, cash and Guaranteed Investment Certificates (GICs) don’t usually match the long-term market returns.

If you don’t want to see that slower growth, you should think of the TFSA as an investment account instead of a savings account. Investors can benefit from long-term compounding by using broad market exchange-traded funds (ETFs) or stocks.

In the past broad-market ETFs have given better long-term TFSA returns than cash or GIC-based methods.

In short the fund has a better chance of making more money over the long term than fixed-income or cash-based methods. Over periods of several decades, TFSA strategies that focus on stocks have done better than those that focus on cash.

People who used this style early on in the TFSA’s history have much bigger balances now.

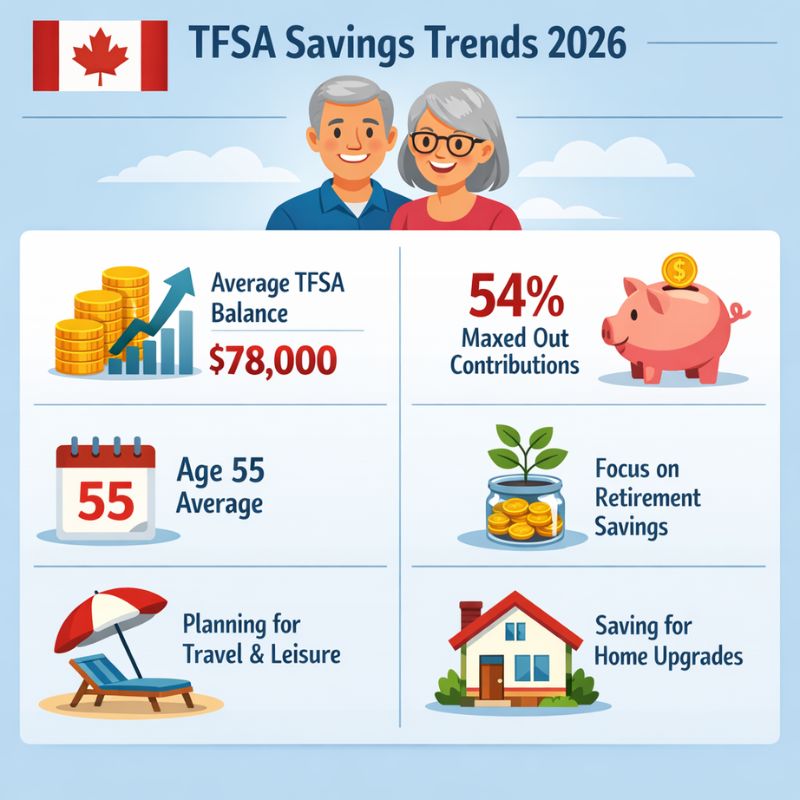

At 55, this is what the average Canadian’s TFSA looks like.

The most recent data from the Canada Revenue Agency (CRA) shows that TFSA balances go up steadily as people get older. Recent filings with the CRA also show that the median TFSA balance rises steadily with age, which shows how the way people contribute affects long-term results.

People in their mid-50s in Canada are at the peak of their earning years, so they usually have the highest median balances of any group.

TFSA balances for Canadians in their 50s tend to be in a wide range. People who have been able to make the most of their contributions since the TFSA started have $117,000 in contribution room.

The average Canadian’s TFSA balance at age 55 is just over $33,000, though. That’s a huge empty space. Even small yearly contributions tend to lead to much better TFSA results by the time you turn 50.

TFSA holders can still look forward to ten more years of deposits, which is good news. There are many ways to close that gap if you choose the right investments for your TFSA, like the Vanguard 500.

Should you put $1,000 into the Vanguard S&P 500 Index ETF right now?

Before you buy shares of the Vanguard S&P 500 Index ETF, think about this:

The Motley Fool Canada team has come up with a list of what they think are the best 10 TSX stocks for 2026. Vanguard S&P 500 Index ETF is not on that list. The 10 stocks that made the cut could make huge profits in the next few years.