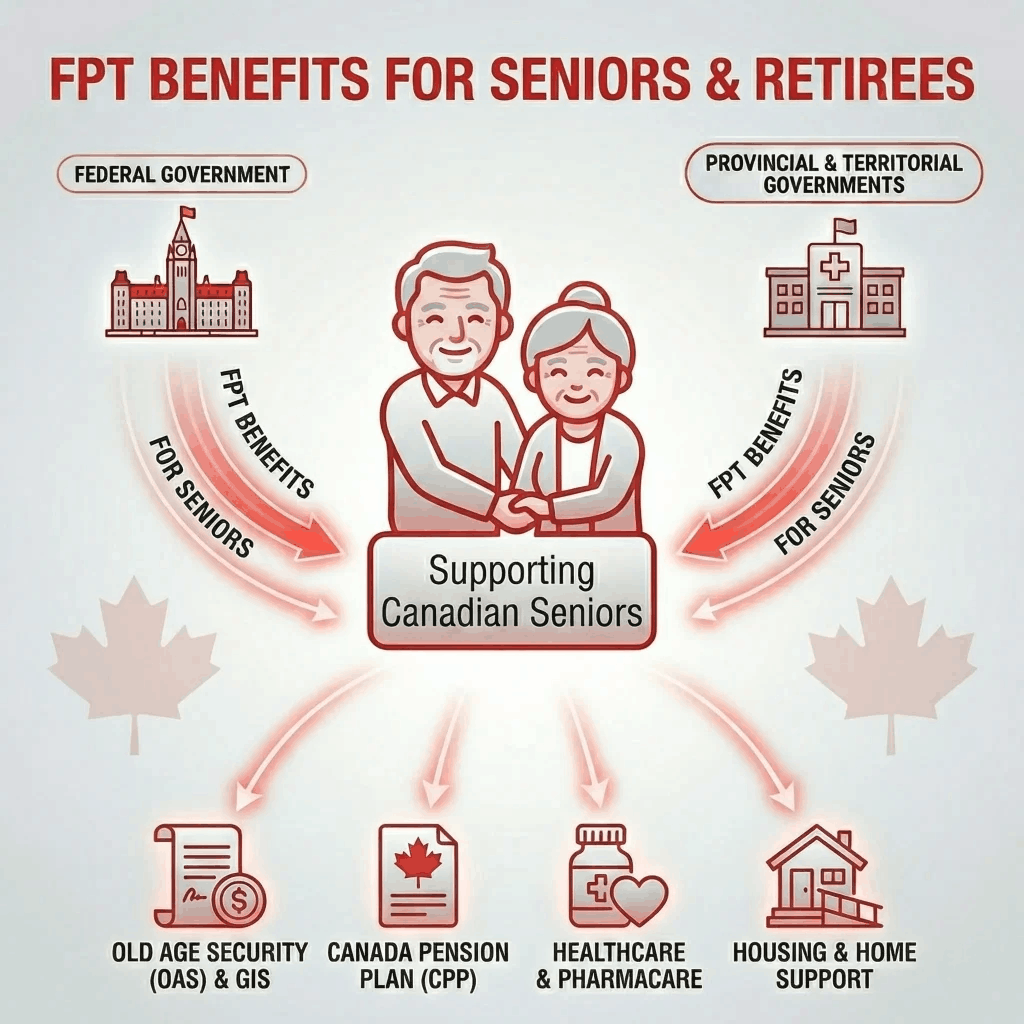

If you’re one of the many seniors in Canada who rely on Old Age Security (OAS) to make ends meet, you’re in luck. In 2026, OAS payments are getting a boost, with an increase in the amount you’ll receive each month. This is part of the government’s effort to adjust payments for inflation and the rising cost of living. So, what does this mean for you? Let’s break it all down in a way that’s easy to understand and helps you make the most of the changes coming this year.

| Key Details | Information |

|---|---|

| 2026 Payment Increase | OAS payments have been increased by 2.1% for the April 2026 quarter. |

| Maximum OAS Amount | Up to $743 for individuals aged 65-74 and $817 for 75+. |

| Payment Schedule | Payments are issued monthly, near the end of each month. |

| Eligibility | Canadian seniors aged 65+ with 10 years of residency. |

| Official Website | OAS page |

In April 2026, you’ll start seeing slightly higher monthly payments from OAS. This increase is a reflection of the government’s commitment to keeping up with inflation and helping seniors maintain their standard of living.

What Exactly is Old Age Security (OAS)?

Old Age Security, or OAS, is a federal benefit designed to provide a basic income to seniors who have lived in Canada. Unlike the Canada Pension Plan (CPP), OAS isn’t based on your contributions during your working years. Instead, it’s based on how long you’ve lived in Canada. So, if you’ve lived here most of your life, you’ll get the maximum benefit, but if you haven’t been in Canada long, you’ll get a reduced amount.

For seniors who have been in Canada for at least 40 years after turning 18, they’ll receive the full OAS benefit. If you’ve lived here for fewer years, you’ll receive a partial benefit, calculated based on how long you’ve been a resident.

2026: What’s New with OAS Payments?

This year, the government is raising OAS payments to help seniors keep up with the rising cost of living. The increase is 2.1% for the April 2026 quarter, which means more money in your account. These increases happen every quarter and are based on the Consumer Price Index (CPI)—essentially the inflation rate.

So, if you’re receiving OAS in April 2026, you can expect a little more in your deposit than usual. This is the government’s way of making sure that the OAS benefit doesn’t lose its value over time.

How Much Will You Receive in 2026?

The amount you’ll receive from OAS depends on your age and how long you’ve lived in Canada. Here’s a rough breakdown:

- For individuals aged 65 to 74, the maximum monthly payment will be around $743.

- For those 75 and older, the maximum payment will increase slightly to $817.

Keep in mind, if you haven’t lived in Canada for the full 40 years, your payments will be lower, but they’ll be pro-rated. So, if you’ve lived in Canada for 20 years, you might get about half of the full amount.

These payments will continue to be sent to you monthly, with most seniors getting their payments toward the end of the month—usually between the 27th and 30th.

Key Dates to Remember in 2026

January 2026: First OAS payment of the year with updated rates.

April 2026: The payments will reflect the increased rate due to inflation.

June 2026: Another quarterly adjustment will take place, based on any further inflation changes.

Who is Eligible for OAS?

To qualify for OAS, you must meet certain requirements. These include your age and how long you’ve lived in Canada. Here’s a quick look at the eligibility criteria:

Age: You need to be at least 65 years old.

Residency: You must have lived in Canada for at least 10 years after turning 18 to qualify. To receive the full benefit, you need to have lived in Canada for 40 years after your 18th birthday.

If you don’t meet the full 40-year requirement, your OAS will be pro-rated. For example, if you’ve lived in Canada for 20 years, you’ll get half the full benefit.

FAQs

Q1: How do I apply for OAS?

If you’re already receiving OAS, you don’t need to apply again. Payments will continue automatically. However, if you’re just becoming eligible, you’ll need to apply through Service Canada, either online or by phone.

Q2: How often are OAS payments adjusted for inflation?

OAS payments are adjusted quarterly to match inflation, so you can expect small increases throughout the year. These changes are based on the Consumer Price Index (CPI).

Q3: Can I get OAS and other pensions at the same time?

Yes! You can receive OAS along with Canada Pension Plan (CPP) benefits or any private pensions you have. Each benefit is separate, so you’ll receive a different amount for each program.

Q4: What happens if I don’t meet the full residency requirement?

If you haven’t lived in Canada for 40 years, your OAS will be reduced based on how long you’ve been here. For example, if you’ve lived here for 20 years, you’ll receive half of the full benefit.

Q5: Will my OAS increase every year?

While the amount can vary, OAS is generally adjusted each year, either quarterly or annually, depending on inflation. This means you can expect gradual increases over time.

How OAS Fits into Your Overall Retirement Plan

While OAS is a great benefit, it’s usually not enough to cover all of your expenses. In Canada, seniors typically rely on a combination of OAS, CPP, and private savings or pensions to make ends meet.

OAS helps ensure that seniors have a basic income, but it’s important to have additional income sources, especially for things like healthcare, housing, and daily living costs.

Tips for Managing Your OAS Payments

Set Up Direct Deposit: This ensures your OAS payments arrive on time every month. You can set it up through Service Canada to avoid delays.

Create a Budget: While OAS provides a steady income, it’s still important to budget your money carefully. Prioritize essential expenses like housing, healthcare, and food.

Look for Extra Help: If your income is on the lower side, check if you qualify for Guaranteed Income Supplement (GIS), which provides additional assistance to low-income seniors.

Save Where You Can: If possible, try to save a portion of your OAS payment for unexpected expenses, such as medical bills or home repairs.

Conclusion

Old Age Security (OAS) is a lifeline for many Canadian seniors, and the increase in payments for 2026 will make a big difference for those on fixed incomes. While it’s an essential source of income, OAS is usually just one part of a senior’s overall financial plan. By understanding how OAS works, setting up direct deposits, and budgeting wisely, seniors can make the most of this important benefit.

Remember to keep track of payment schedules, look into additional support programs, and consider financial planning for the future. For more information, check out Service Canada’s official OAS page or talk to a financial advisor to make sure you’re getting the most out of your retirement benefits.